GUEST POST BY BAILIE SLEVIN: The Asset Trifecta

Please welcome guest poster Bailie Slevin of Entertaining Finance to the blog!

Bailie has a decade of experience as a financial advisor, in addition to having stage managed, general managed, and produced on Broadway and Off-Broadway! Today she’s sharing her tips for financial stability, something we all strive for!

THE ASSET TRIFECTA

OK, miss smarty pants financial adviser, if you have all the answers, where should I put my money?? (I’m betting that’s what you’re thinking now.)

And, really, that’s exactly what you should be thinking! Not to be honest, I’m not actually going to answer the question of where YOU should put YOUR money because I have no freakin clue. I’ve never met you! And even if I had, it would take much more than a cursory conversation to advise you adequately on any financial decision. What I am going to do is give you a way to think about where you want to put your money based on what you want your money to do. And I’m going to use pictures because that makes everything easier to understand.

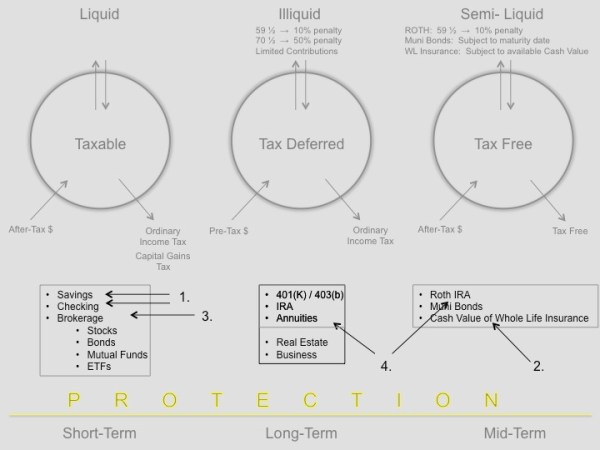

The first way we are going to start to differentiate financial products is by how they are taxed. Now, I am not an accountant. I don’t want to be an accountant. And this is not accounting advice. But this is about tax. In the US there are 3 ways to grow your money:

Taxable, Tax Deferred and Tax Free. (This is the first level of The Trifecta.)

Moving on let’s see how each works.

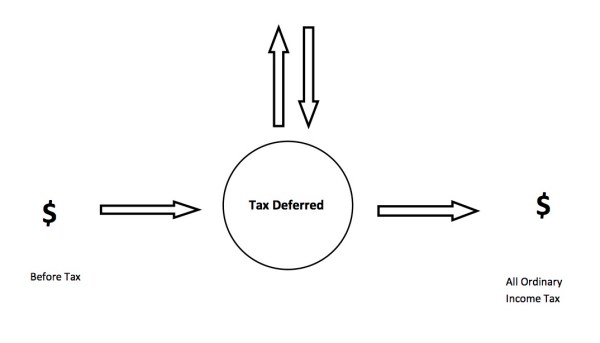

Taxable

Money goes in after tax (for this I mean any money that an employer has paid you that you had income tax taken out of before you even saw it). The money sits in this bucket and hopefully grows. As it grows you get a tax bill on the realized gain (realized gain means the investment is now in some form of spendable dollar and a larger amount then you originally put in). If the money was in the investment for less then 12 months you pay Ordinary Income Tax on the growth (just like on your paycheck). If it was in that sucker for over 12 months you pay Capital Gains Tax which, as of this moment is 15% for people earning under $400,000 a year and 20% for those earning above that number. Check out the diagram. Some examples of this kind of account are savings, checking, stocks, corporate bonds, mutual funds ETFs, brokerage accounts.

Tax Deferred

For this money going in Pre Tax (exactly what it sounds like), you get no tax bill while the money is growing, and when you want to take it out you pay Ordinary Income Tax in whatever tax bracket you are in at the time. This money has some additional rules attached to it.

- If you take the money out of this account before age 59 1/2 you have to pay the tax plus and 10% penalty.

- You must start taking money out of this account starting at age 70 1/2 or you have to pay a 50% penalty on what you should have taken out.

- You are limited on how much you can put in.

Some examples of this kind of account are 401(k), 403(b), IRA, annuity

I tend to call this bucket the tax procrastination bucket since you are, in essence, putting off the tax till tomorrow instead of taking care of it today.

Tax Free

Money goes in here after tax, grows tax free and you can take it out tax free. Boom. There are only three ways to get this done. And each works a little differently.

- ROTH anything – IRA/401(k) – in here there is a limit to how much you can put in. And prior to 59 1/2 you can only take out the money you have put in not any of the growth.*

- Municipal Bonds – depending on where you live and what bonds you buy you could be exempt from all local, state and federal taxes.

- Cash Value of Life Insurance – limit to how much you can put in, attached to life insurance product, could be taxed when you take it out if not done correctly.

So that’s the first level.

The next level to look at is time frame. When you do you want to use this money?

And I’m going really general here so 1 – 10 years, 10 – 20 years, 20 years or more. The taxable bucket has the least restrictions on how and when you can get to your money so that’s the Short Term or 1-10 year bucket, Tax Free has the next highest amount of flexibility so that’s your Mid Term Money (years 10-20) and the Tax Deferred is your Long Term Money since you have to jump through hoops to get at that before age 59 1/2.

The last level is risk. And for that we are first going to get really clear on the difference between saving and investing. Other people may see it differently but here is how it is for me. An account counts as Savings if it is guaranteed never to go down in value unless you take money out. Investments can go up or down in value without you doing anything. Looking at our list of financial products the only ones that are Savings are savings, checking, individual bonds held to maturity and cash value of whole life insurance. Everything else is an investment and therefore has inherent risk. Are some investments riskier then others? Sure! Are we going into that now? No! That is something to be covered with your financial advisor.

Now take a look at the whole picture!!!

OK, so now that we have this strange rubric of The Trifecta, what do we do with it? Well, I’m going to humbly suggest an order.

- Short Term Savings

- Next step is Mid Term Savings

- Short Term Investment

- Mid Term Investment

- Long Term Investment

When you move from step 1 to 2 to 3 to 4 to 5 may vary per person. In fact, it almost definitely will. If you are planning on purchasing a home in the next few years, spend some more time on Short Term Savings. If you have a steady paycheck you may feel more comfortable starting steps 2 and 3 at the same time. The only advice I will give that is for everyone, everyone, everyone – don’t move on to step 4 before you have one years worth of gross income in total between 1,2 and 3. Liquidity, access to you money, is often the only thing standing between you and financial ruin.

Thank you so much, Bailie, for sharing your financial wisdom with us! For more information about Bailie and how her money savvy can help you, check out Entertaining Finance and “like” them on Facebook.